|

Lesson 2

Cash Flow Analysis

A cash flow analysis is just what is says,

a look at how much positive (or negative) cash flow can be expected from a

property. It is not, by itself, really a valuation method, but is

useful fo r determining that the property is worth considering, taking

into

account the loan that you will require. Furthermore, the information

that must be gathered in order to do a cash flow analysis is also often

necessary for completing a full-blown valuation. For small income

properties, for example a single-family home or

duplex, it is more important because the value itself is usually based upon

the comparable sales rather than a method that will analysis income and

expenses. Most of the information required for a cash flow analysis is

also required for a formal valuation. r determining that the property is worth considering, taking

into

account the loan that you will require. Furthermore, the information

that must be gathered in order to do a cash flow analysis is also often

necessary for completing a full-blown valuation. For small income

properties, for example a single-family home or

duplex, it is more important because the value itself is usually based upon

the comparable sales rather than a method that will analysis income and

expenses. Most of the information required for a cash flow analysis is

also required for a formal valuation.

We will look at an example based on a typical

15-year-old 3-bedroom single-family home in Middle Town America. You

will often be able to find shabby looking examples listed for sale with your

favorite broker. Although the price range for our typical home will

vary substantially around the country, we will assume that (1) you are able

to skillfully negotiate a purchase price of $89,000, (2) you expect to

immediately spend an additional $6,000 for rehab, (3) closing costs,

including loan fees, will total $1,200, (4) your combined (federal + state +

local) marginal tax bracket is 22.5 percent, and (5) the rate of

appreciation in your area is 4.3 percent, the average rate over the past 10

years for the 60 largest markets. The rehab will include (1) upgrading

electric and plumbing, (2) painting, (3) re-carpeting, and (4) minor

repairs.

You can usually expect that most lenders will

require 25 to 30 percent down payment on known investment property, so we

will assume 30 percent. Even if the lender will make an 80 percent

loan, the property would then likely have a significant negative cash flow

in most rental markets. Accordingly, our total cash investment will be

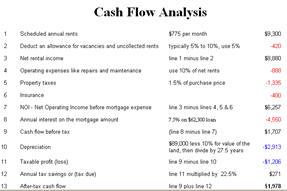

$33,900 ($26,700 + $6,000 + $1,200). The below table shows the remainder of assumptions

for our example and the results of our cash flow analysis. You can

also CLICK

HERE or on the picture of the table below to open the table

in a separate window. You may want to print the table so that you can follow

along with the lesson.

| 1 |

|

Scheduled annual

rents |

$775 per month |

$9,300

|

| 2 |

|

Less allowance

for vacancies & uncollected rents |

typically 5% to

10%, use 5% |

-420

---------

|

| 3 |

|

Net rental

income |

line 1 minus

line 2 |

$8,880

|

| 4 |

|

Operating

expenses like repairs and maintenance |

use 10% of net

rents |

-888

|

| 5 |

|

Property taxes |

1.5% of purchase

price |

-1,335

|

| 6 |

|

Insurance |

|

-400

---------- |

| 7 |

|

Net Operating

Income (NOI) |

line 3 minus

lines 4, 5 & 6 |

$6,257

|

| 8 |

|

Annual interest

on the mortgage amount |

7.5% on $62,300

loan |

-4,550

----------

|

| 9 |

|

Cash flow before

tax |

(line 8 minus

line 7) |

$1,707

|

| 10 |

|

Depreciation |

$89,000 less 10%

for value of the land, then divide by 27.5 yrs |

-$2,913

-----------

|

| 11 |

|

Taxable profit

(loss) |

line 9 minus

line 10 |

-$1,206

|

| 12 |

|

Annual tax

savings or (tax due) |

line 11

multiplied by 22.5% |

$271

|

| 13 |

|

After-tax cash

flow |

line 9 plus line

12 |

$1,978

|

| 14 |

|

Cash-on-cash

return |

line 13 divided

by cash invested $33,900 |

5.8%

|

| 15 |

|

Projected

one-year gain in value or sales price |

For initial

year:

price plus1/2 improvements =

$92,000 times 0.043 |

$3,956

|

| 16 |

|

Projected total

after-tax return for the first year |

Line 13 plus

line 15 |

$5,934

|

| 17 |

|

Total after-tax

overall rate of return for first year |

line 16 divided

by cash invested $33,900 |

17.5% |

|

When

you look at the chart you will see that lines 13 & 14 and lines 16

& 17 tell it all. On line 13, you have the annual after-tax cash

return that you can expect. Line 14 is the calculated rate of return

for the cash that you invest. Lines 16 and 17 tell you what your total

rate of return will be after taking into account the appreciation that

real estate investments have traditionally enjoyed.

|

Keep in mind that we could have picked

parameters so that the results came out to be anything we wanted.

However, we tried to use typical numbers so as to provide typical results.

The 5.8 percent cash-on-cash return isn't great, being about what CDs were

paying early in 2000, but looks good compared to CD rates at the time of

writing this when rates for multi-year CDs aren't much over 3 percent.

The total return, including appreciation, is however more interesting.

Our example produces a reasonable after-tax

return on your investment in rental property the first year, particularly

for a single-family house. Furthermore, the amount of annual interest

decreases each year and adds to your return. Finally, the cash flow

will increase in the future as rents increase and the overall rate of return

in future years should rise substantially because of inflation and leverage (30%

of your money moves 70% of the bank's money).

You may have realized that our rates of

return were lowered because we put $6,000 into the property at the time of

purchase. It seems that buying a property that didn't require this

additional investment would have provided better return. However, then

we would probably have had to pay more for it in the first place, requiring

a larger down payment and larger loan payments. Similarly, buying the

subject property and doing only absolutely necessary repairs (say $500

worth), but no improvements or upgrades, seems like it would improve the

returns. However, this would likely have resulted in lower rents.

The bottom line is that investing in real

estate is as much an art as a science and some decisions are simply a matter

of judgment that comes with experience. It is important that you

utilize analyses like that above to insure that your heart doesn't

override your brain and pocket book when selecting a property to buy.

Keep in mind that you did not get paid for

your work in finding, financing and then managing the property. Single

family rental housing investments may only make sense if you are willing to

work for little or nothing for the first few years that you own them.

However, for many investors with limited resources, they are the only game

in town. We also point out that this analysis shows why you should be

skeptical of claims made by many get rich quick real estate schemes.

There are a other ways to enhance your

after-tax return that are explored in detail in other areas of the e-course

or our Web site. However, if your investment doesn't come close to a

positive cash flow, without tax ramifications, it is probably best to keep

looking unless you can support the negative cash flow for a few years.

|

|

|